In many businesses, the cost of purchasing merchandise for resale (retailing) or the costs of purchasing and converting materials into finished products (manufacturing) represent the business’s most significant expenditures. Keeping track of merchandise and materials, known as inventory, is important because of the considerable costs involved. This can be accomplished through a good inventory record keeping system.

Inventory Record Keeping

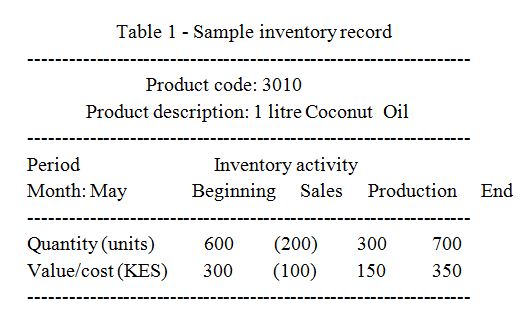

Inventory record keeping establishes and maintains information on current inventory, the additions and withdrawals to inventory and inventory balances at the end of specified periods (week, month, etc.). These records identify the products/materials, the quantities and the value (cost) of these products/materials. A simple inventory record could look like the one shown in Table 1.

The value is the cost of the product. This would be what a retailer paid for the product or what a manufacturer paid for materials plus labor and other charges applied in converting the materials into the finished product. In Table 10, the cost of goods sold would be KES100 for this product for the month of May. There are two different methods used in inventory record keeping: perpetual and periodic.

Perpetual Inventory

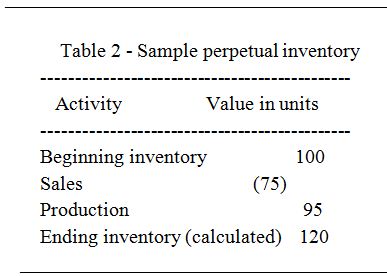

The perpetual inventory method starts with a physical inventory (actual count) and then adjusts this inventory for additions and withdrawals. The inventory at the end of the period is calculated by subtracting the number of units sold from the total of the beginning inventory plus the additional units produced. An example is furnished in Table 2.

The perpetual inventory method is used when reliable sales and production information is readily available and the frequent taking of physical inventories would be burdensome. However, physical inventories must be periodically taken (e.g., quarterly or annually) to check the calculated inventories. The inventory records are then adjusted to agree with the physical inventories. The financial effect of these adjustments is reflected in the balance sheet and the profit/loss statement of the business.

Periodic Inventory

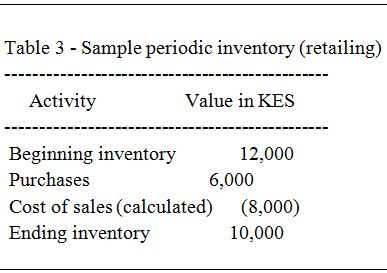

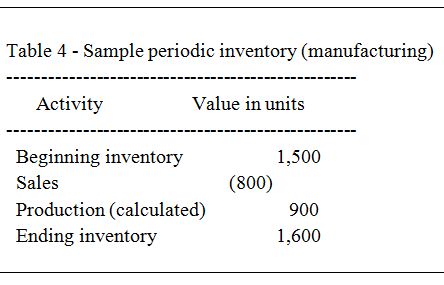

The periodic inventory starts with the physical inventory taken at the end of each period. Sales or production amounts are then calculated based on the beginning and ending physical inventories. This method is used when reliable sales or production data are not readily available. Consider the examples in Tables 3 and4.

In Table3, the cost of sales equals the beginning inventory plus the purchases minus the ending inventory. In Table 4, the number of units produced equals the ending inventory plus sales minus the beginning inventory. Inventory record keeping is primarily used to determine the cost of goods sold as well as to provide information for financial statements.