Procurement Audit Test

Tests of control are tests to obtain audit evidence about the effective operation of the accounting and internal control systems, that is, that properly designed controls identified in the preliminary assessment of control risk exist in fact and have operated effectively throughout the relevant period.

Types of Procurement Audit Tests

Substantive procedures are tests to obtain audit evidence to detect material misstatements in the financial statements. They are generally of two types:

- Analytical procedures

- Tests of detail of transactions, account balances and disclosures

The types of substantive tests carried out to obtain evidence about various financial statement assertions are outlined in the table below.

| Audit assertion | Type of assertion | Typical audit tests |

| Completeness | Classes of transactions

Account balances Presentation and disclosure |

(a) Review of post year- end items

(b) Cut-off testing (c) Analytical review (d) Confirmations (e) Reconciliations to control accounts |

| Rights and Obligations | Account balances Presentation and disclosure | (a) Reviewing invoices for proof that item belongs to the company

(b) Confirmations with third parties |

| Valuation and Allocation | Account balances Presentation and disclosure | (a) Matching amounts to invoices

(b) Recalculation (c) Confirming accounting policy consistent and reasonable (d) Review of post year- end payments and invoices (e) Expert valuation |

| Existence | Account balances | (a) Physical verification

(b) Third party confirmations (c) Cut-off testing |

| Occurrence | Classes of transactions Presentation and disclosure | (a) Inspection of supporting documentation

(b) Confirmation from directors that transactions relate to business (c) Inspection of items purchased |

| Accuracy | Classes of transactions Presentation and disclosure | (a) Recalculation of correct amounts

(b) Third party confirmation (c) Analytical review |

| Classification

And understandability |

Classes of transactions Presentation and disclosure | (a) Confirming compliance with law and accounting

standards (b) Reviewing notes for understandability |

| Cut-off | Classes of transactions | (a) Cut-off testing

(b) Analytical review |

Source: BPP. (2009). Auditing Assurance, ACCA study text

Directional testing

A general assumption that audit firm have is that companies overstate assets and understate liabilities. It also has to do with double entry system e.g. creditors and purchases. If one is correct then most likely the other is correct also.

The techniques used are:

- Review payments after balance sheet date and matching them against related invoices specifically noting dates on invoices to ensure that the invoice was accounted for in the correct accounting period.

- Cut-off tests which involve selecting goods, received notes raised before the year-end and ensuring that the related invoices have been included in the purchases daybook before year-end as well as individual creditors’ accounts. If no invoices have been received to match those goods received notes than a reasonable liability should have been set up.

- Comparison of the present list of creditors with the previous year’s list and investigations being carried out on those creditors on the list of the previous year missing from current year’s list to confirm that they are properly excluded through settlement during the year under review.

- Reviewing reconciliation of creditors’ statements with the creditors’ individual ledger accounts ensuring that any reconciling items are valid and genuine.

- Reviewing lending contracts or agreements for breach of contract accusations to determine where claims would be made against the company.

- Reviewing correspondence with professional advisers e.g. lawyers for claims that they may have made against the company but not recorded.

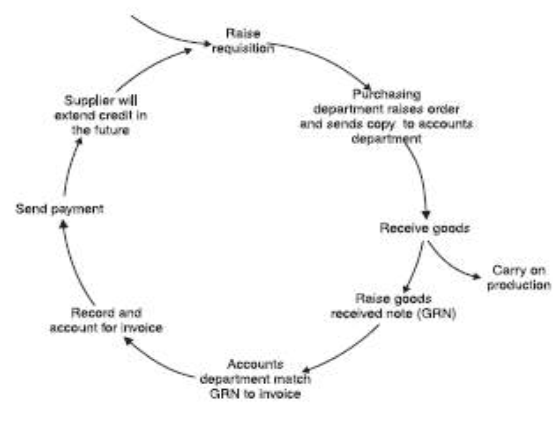

Application of Procurement Audit Tests in Procurement and Inventory Systems

The tests of controls in the purchases system will be based around:

a) Buying (authorization)

b) Goods inwards (custody)

c) Procurement (recording)

Source: BPP. (2009). Auditing Assurance, ACCA study text

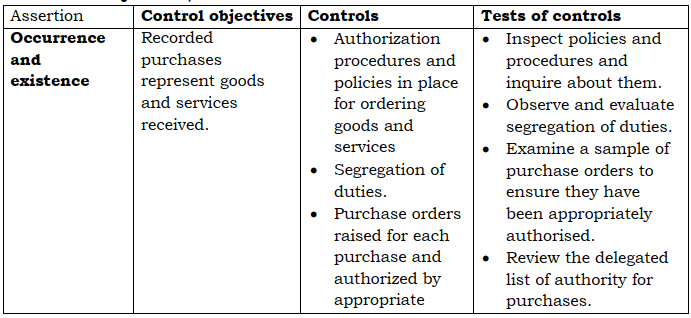

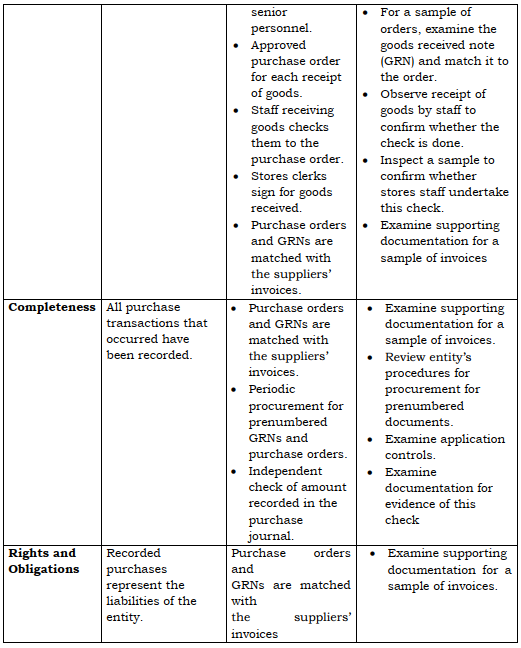

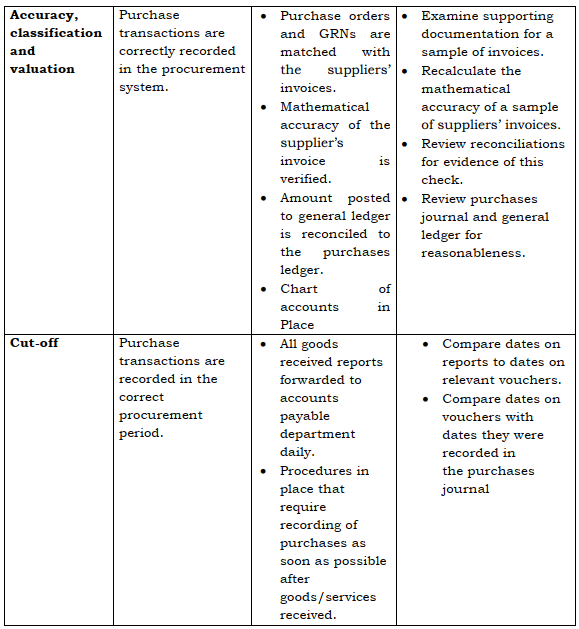

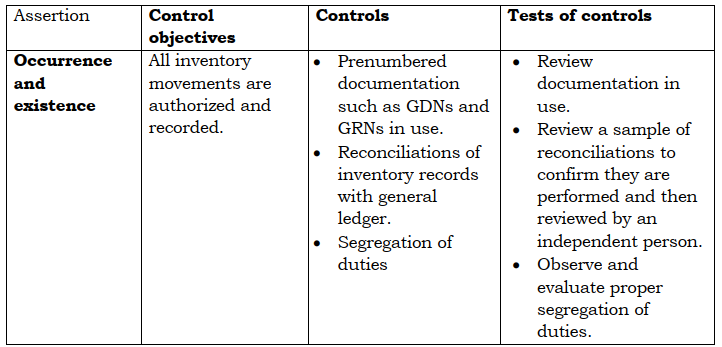

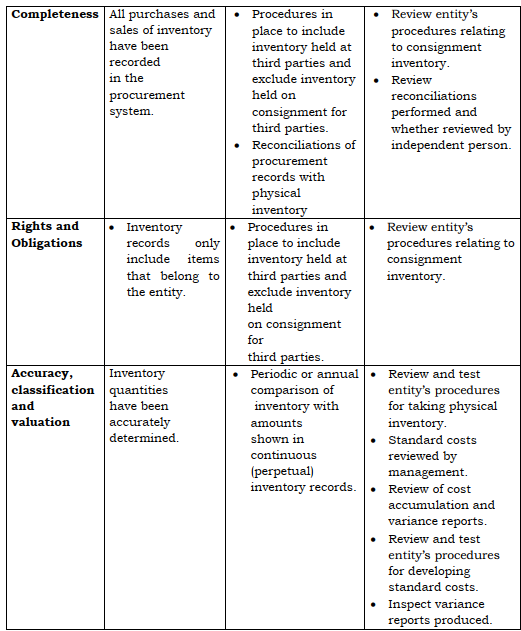

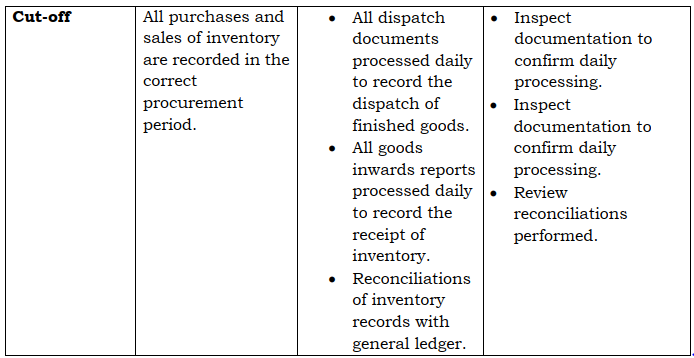

Control objectives, controls and tests of controls

Source: BPP. (2009). Auditing Assurance, ACCA study text

Planning Tests for Procurement Activity

- Compare purchase order prices with vendor catalogs. Variances of significant differences should be investigated.

- Sort payment file by vendor number and amount. These should be investigated to determine if there are duplicate payments for the same invoice

- Spot check receiving. Periodically, examine products being received by the company. This verifies the items received have been ordered, and are consistent with what a normal business orders.

- Probe for favored vendors. Purchase order file sorted by vendor number. The frequency of vendor orders should be accumulated and ranked. Vendors receiving large amounts of orders should be investigated to determine that price and service offered is competitive with other vendors

- Validate adequate segregation duties. Document the duties of individuals and analyze the results to make sure adequate segregation exists.

- Compliance to procedures. Select a random number of purchase orders to verify that all of the appropriate procedures were complied with in processing and recording the purchase order.

- Verify that the requestor has proper authorization to order the products.

- Check the vendor invoice for the following: Clerical accuracy, Proper dates, Propriety of account distribution, Appropriateness of purchase.

- End-of-month liability analysis. Items entered as liabilities immediately following the end of the accounting period should be examined to determine whether they have been recorded in the proper accounting period.

- Purchase needs audit. Objective is to determine whether the item purchased already exists in the company and could be used without repurchasing

Question Purchase controls

GDC, a limited liability company, operates a computerized purchase system. Invoices and credit notes are posted to the purchases ledger by the purchases ledger department. The computer subsequently raises a cheque when the invoice has to be paid.

Required

List the controls that should be in operation:

(a) Over the addition, amendment and deletion of suppliers, ensuring that the standing data only includes suppliers from the company’s list of authorised suppliers

(b) Over purchase invoices and credit notes, to ensure only authorised purchase invoices and credit notes are posted to the purchase ledger

Answer

(a) Controls over the standing data file containing suppliers’ details will include the following.

(i) All amendments/additions/deletions to the data should be authorised by a responsible official. A standard form should be used for such changes.

(ii) The amendment forms should be input in batches (with different types of change in different batches), sequentially numbered and recorded in a batch control book so that any gaps in the batch numbers can be investigated. The output produced by the computer should be checked to the input.

(iii) A listing of all such adjustments should automatically be produced by the computer and reviewed by a responsible official, who should also check authorization.

(iv) A listing of suppliers’ accounts on which there has been no movement for a specified period should be produced to allow decisions to be made about possible deletions, thus ensuring that the standing data is current. The buying department manager might also recommend account closures on a periodic basis.

(v) Users should be controlled by use of passwords. This can also be used as a method of controlling those who can amend data.

(vi) Periodic listings of standing data should be produced in order to verify details (for example addresses) with suppliers’ documents (invoices/ statements).

(b) The input of authorized purchase invoices and credit notes should be controlled in the following ways.

(i) Authorization should be evidenced by the signature of the responsible official such as the Chief Accountant. In addition, the invoice or credit note should show initials to demonstrate that the details have been agreed: to a signed GRN; to a purchase order; to a price list; for additions and extensions.

(ii) There should be adequate segregation of responsibilities between the posting function, inventory custody and receipt, payment of suppliers and changes to standing data.

(iii) Input should be restricted by use of passwords linked to the relevant site number.

(iv) A batch control book should be maintained, recording batches in number sequence. Invoices should be input in batches using pre-numbered batch control sheets. The manually produced invoice total on the batch control sheet should be agreed to the computer generated total. Credit notes and invoices should be input in separate batches to avoid one being posted as the other.

(v) A program should check calculation of sales tax at standard rate and total of invoice. Nonstandard sales tax rates should be highlighted.

The Inventory System

Inventory controls are designed to ensure safe custody. Such controls include restriction of access, documentation and authorization of movements, regular independent inventory counting and review of inventory condition.

The inventory system can be very important in an audit because of the high value of inventory or the complexity of its audit. It is closely connected with the sales and purchases systems covered in the previous sections.

There are three possible approaches to the audit of inventory and the approach chosen depends on the control in system in place over inventory.

(a) If the entity has a perpetual inventory system in place where inventory is counted continuously throughout the year, and therefore a year-end count is not undertaken, a controls-based approach can be taken if control risk has been assessed as low.

(b) If an inventory count is to be undertaken near the year-end and adjusted by perpetual inventory records for the year-end value, this approach also requires control risk to be assessed as low.

(c) If inventory quantities will be determined by an inventory count at the year- end date, a substantive approach is taken and no reliance is placed on controls. Control objectives, controls and tests of controls

Most of the controls testing relating to inventory has been covered in the purchase and sales testing outlined in sections 1 and 2. Auditors will primarily be concerned at this stage with ensuring that the business keeps track of inventory.

Source: BPP. (2009). Auditing Assurance, ACCA study text